The first, and most essential, step toward obtaining federal financial aid is completing a Free Application for Federal Student Aid (FAFSA).

The FAFSA has existed for over 30 years, but Congress and the Department of Education completely overhauled the 2024-2025 FAFSA.

While the rollout has been rough and has caused delays that extend into the 2025-2026 aid year, this comprehensive guide will help you find your way.

In This Guide

- FAFSA Overview

- Types of FAFSA Aid

- FAFSA Process & Changes

- Deadlines & Timeline

- Additional Options

- Conclusion

What is the FAFSA?

The FAFSA is the national application for all students who wish to receive federal financial aid in the U.S., including grants, student loans, and work study.

In addition, the information on the FAFSA determines eligibility for many state grants, institutional grants and scholarships, and other aid.

- Citizens and permanent residents, as well as select eligible non-citizens of the U.S., are eligible for federal financial aid via the FAFSA.

- Students must have a high school diploma or GED, enroll in an eligible program, and maintain satisfactory academic progress.

- In addition, students who have received federal aid previously must not be in default on their student loans and must not exceed the annual and lifetime limits of aid.

Types of Aid Offered through the FAFSA

Federal grants include the Pell grant and Supplemental Educational Opportunity Grant (SEOG). The Pell grant and SEOG are based on financial need as determined by the FAFSA.

In prior years, the Expected Family Contribution (EFC) determined eligibility, but with the changes to the 2024-2025 FAFSA the number used to calculate aid is now the Student Aid Index (SAI).

Grants and scholarships are the most beneficial type of financial aid because they do not require repayment. Many states also offer grants and scholarships based on information provided on the FAFSA.

In addition to grants, the FAFSA enables students to access federal student loans.

There are two types of federal student loans: subsidized and unsubsidized. The difference between these loans is that the subsidized loan does not accrue interest while you are attending college at least half time.

The unsubsidized loan does accrue interest from the time it disburses. For this reason, some students accept subsidized loans but decline unsubsidized loans if their financial situation allows them to do so.

Students may be more aware of student loans and concerns about student loan debt due to additional publicity lately, but there are definite benefits to using student loans to cover tuition costs if you do not have another way to cover them.

If you need to borrow funds to help pay your tuition, student loans offer relatively low interest rates and flexible repayment plans that make them far superior to most private loans, and infinitely better than using a credit card.

Understanding student loan interest rates

For undergraduate student loans disbursed between July 1, 2024, and July 1, 2025, the current fixed interest rate is 6.53%, and an origination fee of 1.057% is subtracted from the loans when they disburse.

While Congress may change interest rates for student loans each year when they renew the federal budget, the interest rate on loans you already have will not change.

For more information about student loan interest rates and fees, you can visit the interest rate page of studentaid.gov for the most accurate and up-to-date information.

Student loans enter the repayment phase six months after you leave school (or reduce your attendance to less than half time).

When repayment begins, the new SAVE program offers income-driven repayment, so payment amounts are based on the income of the debtor. Through this program, some students will have payments set at $0 per month until their income increases.

In addition, there are loan forgiveness programs available for students who major in certain areas of study (teaching, nursing, etc.).

The third type of aid offered via the FAFSA is Federal Work-Study. This aid is in the form of income earned through a (usually part-time) work study job. Federal Work Study is financial aid because the federal government subsidizes the student’s wages. This makes finding employment easier, because employers don’t have to cover the full wages for the student.

FAFSA Process & Changes

Students complete the FAFSA online at studentaid.gov.

Federal Student Aid redesigned the website to be mobile-friendly, in addition to its traditional computer format, so many students complete the FAFSA using a smartphone.

You will need to create an account at studentaid.gov at least three days prior to the day you plan to complete the FAFSA. This account is your Federal Student Aid account, or your Federal Student Aid Identification (FSA ID). In addition, any other contributors must also create an FSA ID at least three days before completing their portion of the FAFSA:

- A contributor is someone who is required to contribute information to the FAFSA for a student to be eligible for aid.

- The student is a contributor.

- Married but not separated students must include their spouse as a contributor.

- Dependent students must include at least one parent as a contributor. The FAFSA contains “Personal Circumstance” questions to help determine whether a student is considered dependent, but generally, any undergraduate student who is under the age of 24, has not served in the military, and is unmarried with no dependents is dependent if they have a relationship with their parent(s).

To view the questions used to determine whether a student is independent or dependent, please visit the dependency section of studentaid.gov. Please note that the questions currently available at the site are for the 2025-2026 FAFSA.

The first question for 2024-2025 asked if the student was born before January 1, 2001, and other questions had similarly adjusted dates.

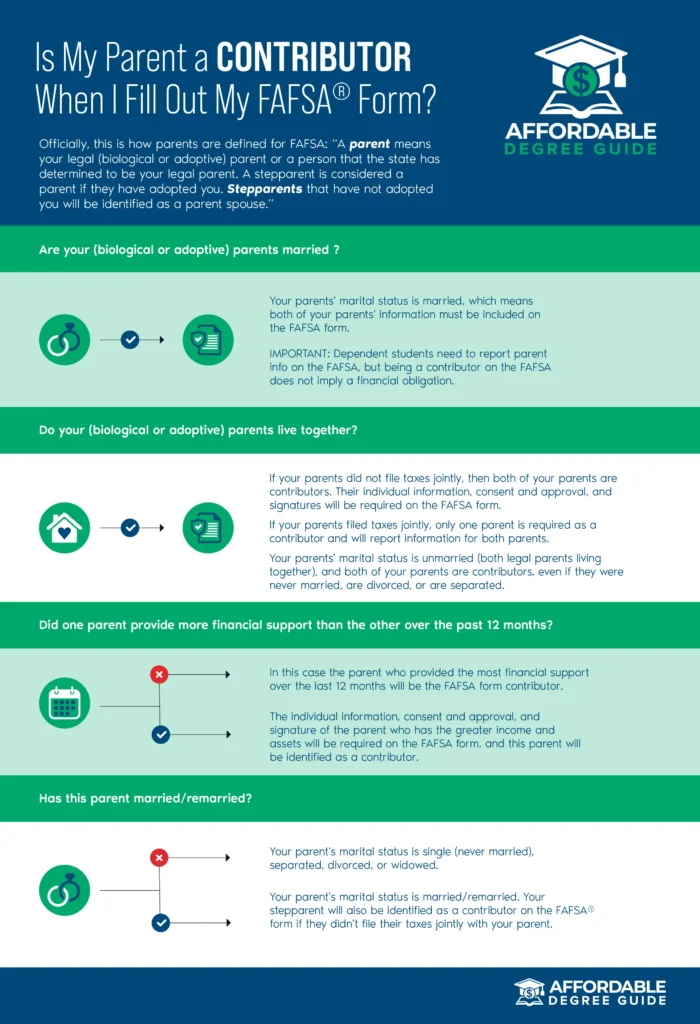

Like so many things, the method for determining which parent a dependent student should use on the FAFSA changed with the 2024-2025 aid year. The flowchart below explains how to determine which parent to use as a contributor. These rules for identifying parent contributors are the same for the 2025-2026 FAFSA. An online Parent Wizard feature is now available at https://studentaid.gov/fafsa-apply/parents to help dependent students determine which parent(s) to use on the FAFSA.

SOURCE: https://studentaid.gov/2425/help/which-parent-contributor

Each FAFSA year uses the tax and income information from two years prior. Therefore, the 2024-2025 FAFSA uses tax and income information from 2022, and the 2025-2026 FAFSA uses tax and income information from 2023.

With the recent changes to the FAFSA, most income information for contributors imports from the Internal Revenue Service (IRS), and contributors must give permission for the IRS to share tax information with the Federal Student Aid (FSA) on the FAFSA.

As a result, contributors frequently no longer need to add tax information manually to complete the FAFSA, but FSA recommends that you and other contributors have your taxes for the appropriate year on hand just in case.

Any contributors who did not file taxes for the tax year used by the current FAFSA, but who did have income from working, should have their W2s for that year available. In addition, all contributors should have records ready for any untaxed income, including child support, and assets, such as bank accounts, investments, businesses and farms from the appropriate year.

Because the IRS now imports tax information for most contributors, schools will not need to ask for tax information for verification purposes as often, but FSA has not eliminated verification, and schools must clear any conflicting information, so your school may request a tax return transcript. If they do, you can request it online at the IRS website for immediate download.

Usually, Federal Student Aid opens a FAFSA for completion October 1 of the year prior to when students will need it to attend college. However, because of the recent overhaul of the FAFSA, the 2024-2025 FAFSA was not available for student completion until months later.

The release of the 2025-2026 FAFSA was also delayed, but it has been open to students since November 21. Find more information on the 2025-2026 FAFSA rollout.

Common Mistakes to Avoid

Frequently, when students and other contributors have trouble completing the FAFSA, it is because they have entered information incorrectly. This starts with the FSA ID.

Each person who creates an FSA ID must be careful to use their legal name from their Social Security card and be careful to avoid typos in the Social Security number (SSN), date of birth, and email address.

For example, if a student attempts to invite a parent to contribute information to the FAFSA, but the student enters a typo in the parent’s name, SSN, or date of birth, the system will be unable to match the contributor to the student, and the contributor will not receive the invitation to complete.

For contributors who do not have an SSN, the FSA system uses mailing address information to match them to the student, so the student must enter the contributor’s address in a format identical to the address reported in that contributor’s FSA account profile. If the format doesn’t match exactly, the invitation will not go through.

Providing correct marital status information is critical to completing a FAFSA and, as odd as it may sound, there are frequent errors involving marital status.

The marital status “single,” is for people who have never married, so people who are separated or divorced from a spouse should not use it. Parents of dependent students who are unmarried but live together must both contribute information to the FAFSA. Please be sure to read all marital status options carefully before responding, and if you are not sure about your parent’s marital status, ask them before responding.

Starting with 2024-2025 FAFSA, all contributors must give permission for the IRS to share tax and income information with FSA, even if they did not file taxes. If a contributor does not give permission for this information sharing, the student will not be eligible for federal aid.

Even if you don’t think you are eligible for federal aid due to income, complete a FAFSA. Schools frequently use information from the FAFSA to determine whether you are eligible for state aid or institutional aid, and even if you are not eligible for grants or scholarships, the FAFSA gives you access to federal student loans, which may help you manage the expense of your tuition.

Deadlines & Timeline

The deadline for completing the 2024-2025 FAFSA is June 30, 2025. The deadline for completing the 2025-2026 FAFSA is June 30, 2026.

It may seem like there’s no rush if the FAFSA deadline is so far away but putting it off is a bad idea. As soon as the FAFSA is available for completion, get it done.

Complete your FAFSA and provide any requested information to the school as quickly as possible, to maximize your financial aid eligibility. Some funds have limits and are available to students on a first-come-first-served basis. If your school requests information from you, respond promptly. Schools must follow federal regulations to award financial aid, and if you don’t provide what they need, you may lose that financial aid.

In addition, you need to have the FAFSA done in time to receive any state grants and scholarships. Many states have grant and scholarship deadlines early in the year, frequently as early as Jan. 31. If you fail to complete your FAFSA by your state’s deadline, you will not receive funds from your state.

Additional options

If you feel that the income and exemption information shared by the IRS on your FAFSA are significantly different from your current income situation, such as, if a parent of a dependent student is currently unemployed or had a significant income decrease since the tax year used, talk to the financial aid office at your school.

Financial aid professionals are sometimes able to change income information on the FAFSA as part of an appeal process, and they will tell you what steps to take to have your file reviewed.

In addition, if you are a dependent student with unusual circumstances that make it difficult or impossible to get parent information for the FAFSA, discuss this with your school’s financial aid office. They may be able to assist you.

Conclusion

Completing your FAFSA is the most critical step you can take toward preparing to fund your college-level courses.

Take it seriously.

Take it slow, set aside time to focus, have your documents ready, and make sure everything is correct. This will save you from frustration and other problems later. Whether you attend a public university, a private college, or a trade school, the FAFSA is essential in helping you afford to achieve your educational goals.